Join our daily newsletter At The Bell to receive exclusive market insights

Gold commands almost universal wonder for consumers and investors alike, but it also holds a practical role in a diversified investment portfolio. While physical holdings may once have been the only option for direct investment, or using gold mining stocks as a proxy, ETFs have made this commodity more accessible than ever to investors globally. A range of geopolitical risks in the global economy, along with the globally low interest rate environment, have made gold increasingly relevant and valuable in a portfolio, as both a hedge for market volatility and a source of growth.

The beauty of gold

Gold is traditionally viewed as a safe haven investment for its low (and at times, negative) correlation to other asset classes, along with its ability to typically offer positive performance in volatile periods.

Table 1 below shows the correlations between gold and major asset classes over 20 years.

Table 1:

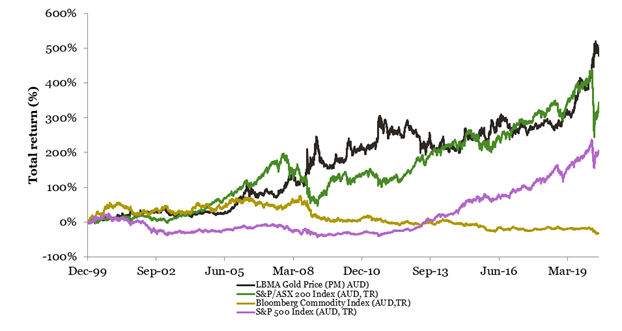

This relationship means gold can be more than just a safe haven in sharemarket volatility, it can also offer diversification against all asset classes. Its ability to perform in all markets as both a consumer-driven as well as investment-driven asset means it has both defensive and growth characteristics. Chart 1 below shows how gold has been able to offer solid returns over the long-term, comparable to other growth assets like equities and commodities, and outperforming fixed interest and cash.

Chart 1:

Source: Bloomberg, ETF Securities 31 December 1999-31 May 2020

As part of a diversified portfolio, gold might typically represent between 2-10% of an allocation, depending on an investor’s needs or strategy, but many investors are missing this allocation. This may partly be due to a lack of understanding of how gold works in a portfolio and partly due to a lack of awareness of the options for access.

Accessing gold using an ETF

The traditional forms of access to gold were either through physical holdings or an indirect exposure by owning shares in gold mining companies. Both had their challenges – physical holdings namely through prohibitive costs and indirect exposure by opening to assorted company risks. Generally speaking, physical holdings were preferable to mining companies as a pure exposure.

The first gold-backed ETF was launched in 2003 by ETF Securities, it still trades today as ETFS Physical Gold (ASX:GOLD) and held $1,692 million in assets as at 12 June 2020. Gold-backed ETFs are literally as described, where physical gold is purchased and stored by a fund manager as part of a trust and investors buy units in the trust for exposure to the market movements of gold.

Using an ETF for gold exposure has several features and advantages over the physical holdings.

Cost tends to be a foremost consideration.

To buy physical gold, investors tend to need to pay a premium over the spot price. Investors in physical gold may also need to consider freight costs, storage and insurance costs. These costs may exclude many investors from access.

By contrast, as a unit holding exposure rather than physical ownership, ETFs are cheaper to access and costing a percentage of the spot value of physical gold. For example, ASX: GOLD costs roughly 10% of the spot price of gold (based on the LBMA Gold Price PM). There are also ongoing management fees to cover storage and insurance. These management fees also tend to be cheaper than physical storage and insurance costs. In the case of GOLD, this is 0.40% annually.

The liquidity and ease of use of gold-backed ETFs compared to physical gold is another consideration. Investors holding ETFs may be more able to adjust their holdings to reflect activity in the market, selling when they see a particular price with a click compared to those holding physical holdings which may take longer to buy and sell. This can be a challenge for some investors depending on their investment horizon and levels of risk-aversion.

ETFs are also typically easier to use compared to physical gold holdings, requiring as little as a trading account to get started and can be done anywhere. It can be less intimidating for many investors who may not be aware of even where to start for physical purchasing and trading.

Understanding the risks

As an investment tool, ETFs are subject to a range of general investment risks, such as market risk or counterparty risk.

Market risk relates to loss of value due to movements in the overall share market. Given gold-backed ETFs typically track the spot price of gold and this is less correlated to equity markets, the risk is somewhat reduced. Whether physical gold or gold-backed ETFs though, investors are subject to the movements in gold prices which can mean gains or losses based on the difference between purchase or sale prices.

Counterparty risk is the risk that the other party to your investment defaults or mismanages your assets. For example, the risk that the custodian holding the physical gold (whether for an ETF or individual investor) has not securely stored the gold and it is stolen or lost. Custodians of assets held in managed funds, like ETFs, typically hold insurance to cover the risk of loss or theft but investors using physical assets may need to investigate their own insurance options. Another example might occur at the time of investment purchase – if the trading tool or company doesn’t actually use your funds to buy the selected investment or asset. Using established and credible companies to purchase investments can be an important way of managing this risk.

There can also be variation in the way that gold-backed ETFs are managed, so investors should research their options. For example, while ASX:GOLD can be redeemed for the physical holdings, and investors are entitled to their share of the holdings, some gold-backed ETFs only give investors a cash entitlement. A cash entitlement may be a risk for those investors concerned about financial markets and the stability of financial companies.

Physical holdings of gold hold their own risks, such as liquidity risk or the risk of theft. Liquidity risk is the risk that the physical holding can’t be sold as quickly as an investor needs due to market demands. Investors will need to weigh up the risks of either before deciding to buy physical gold or a gold-backed ETF.

For the ages

Unlike many themes and investment cycles, gold is for the ages. It is a long-term investment and worth considering as part of the core of a portfolio for its ability to offer diversification, growth and a measure of stability over time. While ETFs have made gold exposure more accessible than ever before, features like liquidity and ease of use make them an appealing option for a broad range of investors to consider in a portfolio.

Disclaimer

This document is communicated by ETFS Management (AUS) Limited (Australian Financial Services Licence Number 466778) (“ETFS”). This document may not be reproduced, distributed or published by any recipient for any purpose. Under no circumstances is this document to be used or considered as an offer to sell, or a solicitation of an offer to buy, any securities, investments or other financial instruments and any investments should only be made on the basis of the relevant product disclosure statement which should be considered by any potential investor including any risks identified therein.

This document does not take into account your personal needs and financial circumstances. You should seek independent financial, legal, tax and other relevant advice having regard to your particular circumstances. Although we use reasonable efforts to obtain reliable, comprehensive information, we make no representation and give no warranty that it is accurate or complete.

Investments in any product issued by ETFS are subject to investment risk, including possible delays in repayment and loss of income and principal invested. Neither ETFS, ETFS Capital Limited nor any other member of the ETFS Capital Group guarantees the performance of any products issued by ETFS or the repayment of capital or any particular rate of return therefrom.

The value or return of an investment will fluctuate and investor may lose some or all of their investment. Past performance is not an indication of future performance.

Information current as at 15 June 2020.